In a complex loan origination environment, misrepresentations and document defects are frequently buried deep within routine paperwork. Subtle issues like altered numerical fields on a pay stub, inconsistent employer names, or missing pages introduce significant hidden risk into a lender’s pipeline. Catching these anomalies across hundreds of pages places an immense operational burden on risk teams, prompting the mortgage industry to shift toward intelligent document automation backed by strict regulatory frameworks.

This technological evolution is underscored by major housing entities setting new benchmarks for adoption. A primary example is highlighted in the Fannie Mae Launches AI Fraud Detection Technology Partnership with Palantir announcement, which introduced an AI-powered unit to scan massive datasets for previously undetectable patterns. This institutional shift was further codified in April 2026 when Fannie Mae issued Lender Letter LL-2026-04, detailing strict governance requirements for utilizing machine learning engines within originations.

However, these advanced automated systems do not replace experienced human judgment. Instead, AI serves as a protective analytical assistant within an Intelligent Document Processing (IDP) framework, helping risk professionals isolate potential inconsistencies and data conflicts with greater precision, clarity, and speed.

What is Mortgage Fraud Detection AI?

Mortgage fraud detection AI refers to the strategic application of machine learning, optical character recognition, natural language processing, and advanced document intelligence to identify suspicious patterns, data inconsistencies, and potential misrepresentations within loan files. Rather than relying solely on manual, visual checks by a human processor, mortgage fraud detection AI analyzes text layers, structural layouts, and document metadata to flag potential risk indicators for further human evaluation.

It is critical to note that these AI systems do not independently determine that fraud has occurred. They do not possess the legal or operational authority to make a final fraud declaration, nor do they replace the necessary investigatory workflows of fraud prevention teams. Instead, the technology serves as an automated analytical assistant. It flags anomalies, uncovers hidden data mismatches, and surfaces hidden document risks so that qualified mortgage professionals can conduct focused, deeper investigations.

Why is Mortgage Document Fraud Difficult to Detect Manually?

A single mortgage loan application requires an extensive array of documentation. Processing and underwriting teams must evaluate pay stubs, W-2 forms, federal tax returns, bank statements, personal identification documents, purchase contracts, asset verification statements, gift letters, and disclosures. Reviewing this massive volume of unstructured and semi-structured paperwork is highly time-consuming and prone to human oversight.

Manual reviews can easily miss micro-level inconsistencies. For instance, an altered income figure might be printed in a font that matches the rest of the document perfectly to the naked eye but contains tiny pixel variations or structural alignment anomalies. Similarly, an applicant might submit an asset statement where a single page containing a large, unverified transfer has been intentionally omitted.

Other common operational challenges include:

- Template Exploitation: The reuse of legitimate document templates updated with modified transaction dates

- Nomenclature Discrepancies: Mismatched employer names across different tax, asset, and income forms

- Historical Variances: Subtle, erratic variations in historical transaction patterns within deep bank statements

Expecting underwriters to spot every minor discrepancy across thousands of document pages weekly creates an unsustainable operational bottleneck that directly impacts time-to-close.

How is AI used in Mortgage Fraud Detection?

To answer the central industry question, ‘How is AI used in mortgage fraud detection?’, it helps to examine how automated systems break down and analyze loan files. Instead of viewing a document as a static image, an AI platform treats it as a complex network of data points, layouts, and historical patterns. While global financial frameworks might rely on general tools, such as the broad AI fraud detection banking systems utilize for credit cards or merchant risk, the US residential mortgage market requires a highly specialized, document-focused intelligence layer.

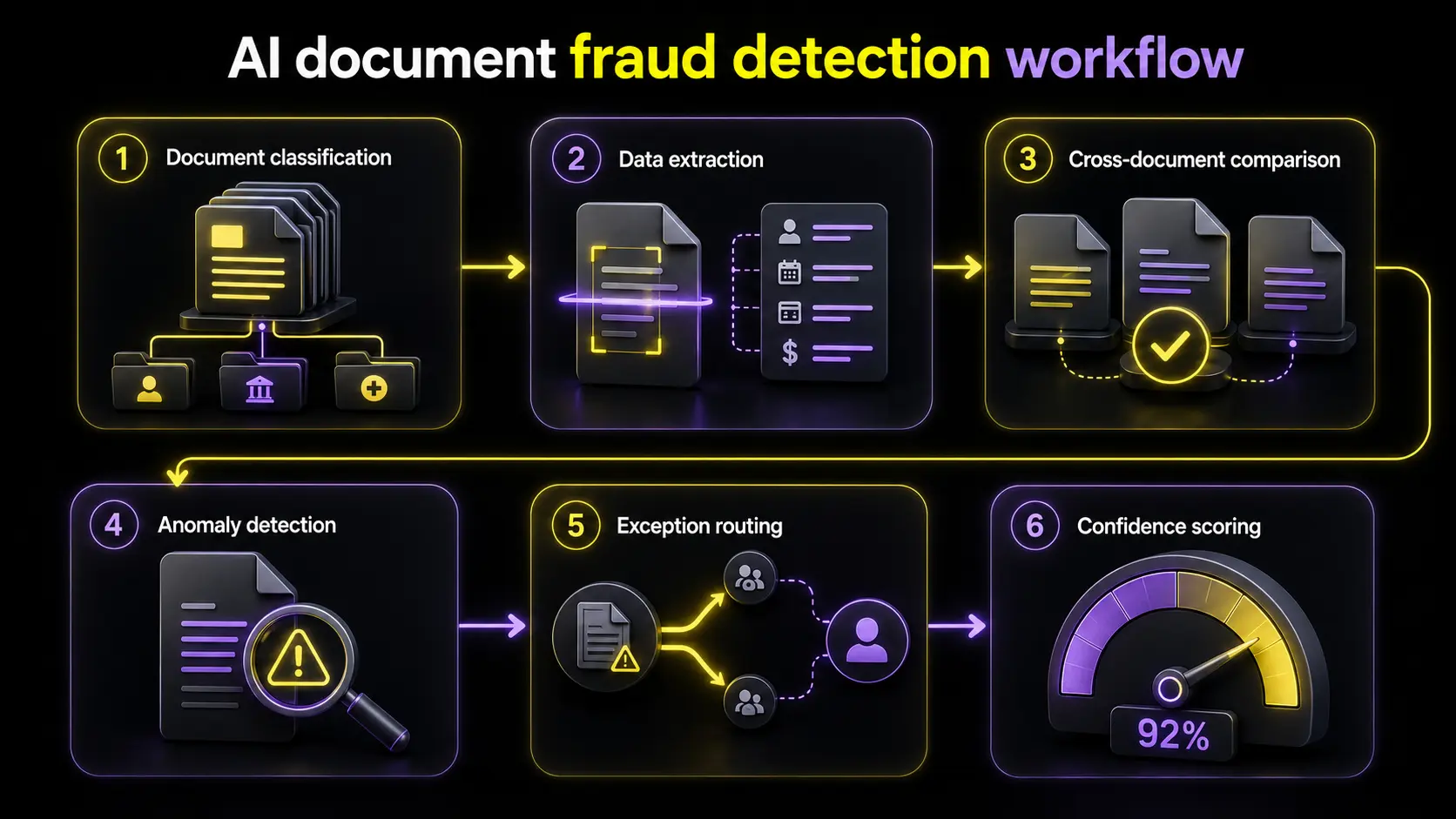

The process operates through several integrated structural stages:

Document Classification

The system automatically identifies the exact type of each document uploaded, distinguishing a 1040 tax form from a W-2 or a multi-page bank statement without human intervention. This ensures that the correct validation rules are applied instantly.

Data Extraction

Advanced machine learning algorithms extract critical text and numeric values from specific fields, turning unstructured images into organized digital data for verification.

Cross-document Comparison

The technology compares extracted data across multiple files. For example, it cross-checks the gross income listed on a pay stub against the year-to-date earnings on a W-2 and the actual deposits shown on a bank statement to improve data consistency and identify structural data inconsistencies.

Anomaly Detection

The system reviews the structural composition of the document itself, flagging unusual layouts, font mismatches, or altered metadata that suggest digital editing.

Exception Routing

When an inconsistency or risk indicator is identified, the system automatically routes the file to a specialized fraud or senior underwriting team for closer review.

Confidence Scoring

Every extraction and validation check receives a confidence score. Low scores signal to the team that a human eye must verify the information.

Human Review

The final step always relies on a mortgage professional who evaluates the flagged risks and makes the final operational decision on how to proceed.

Can AI Detect Forged Documents?

When risk management teams ask, ‘Can AI detect forged documents?’, the answer requires a careful understanding of software capabilities. A system utilizing forged document detection AI cannot definitively declare a document a forgery in a legal sense, but it is highly effective at identifying the technical indicators of potential alteration.

Forged document detection AI inspects files for microscopic and structural irregularities that humans often overlook. This includes analyzing the document’s digital metadata for signs of image editing software, detecting mismatched font styles or sizes within a single line of text, and identifying white-out or text-layer overlays.

Furthermore, AI can flag duplicated document templates, such as when two entirely different applicants submit bank statements with identical transaction histories or serial numbers. By uncovering these formatting irregularities, missing pages, and conflicting data points, the technology alerts lenders to files that require comprehensive, manual verification.

How do Lenders Identify Fake Loan Documents?

In daily practice, how do lenders identify fake loan documents while keeping originations moving efficiently? Modern operations teams use a multi-layered verification strategy that combines automated document analysis with traditional verification workflows.

A robust framework for fake document detection in loan processing incorporates several practical review methods:

- Cross-document comparison: Lenders verify perfect alignment between the borrower’s application details, employer documentation, bank transcripts, and federal tax records

- Consistency inspections: Automated checks evaluate whether reported year-to-date earnings mathematically match the frequency and amount of verified bank deposits

- Transactional pattern analysis: Systems analyze bank statement histories to ensure that monthly opening and closing balances calculate correctly based on listed deposits and withdrawals

- Completeness audits: Rules verify that multi-page documents contain all sequential pages and that no critical sections or disclosure addendums have been removed

- Visual formatting scans: Processing software and underwriters inspect text alignments, font weights, corporate logos, and borders for signs of digital manipulation

- Targeted exception routing: Any document failing automated validation triggers is automatically flagged and escalated to senior risk investigators

- Audit trail maintenance: Systems log all automated flags and subsequent human decisions to demonstrate compliance during quality control audits

Where does Intelligent Document Processing fit within Risk Workflows?

Intelligent Document Processing (IDP) serves as the core operational foundation that makes mortgage fraud analytics scalable. Without IDP, document data remains locked inside static PDFs, scanned images, and multi-page uploads, making advanced analysis nearly impossible.

IDP technologies convert unstructured and semi-structured mortgage documents into highly organized, review-ready digital information. By serving as a foundation for loan document automation, an IDP platform enables automated validation systems to look across the entire loan file instantly, creating a fast track for automated mortgage processing.

Features like confidence scoring allow the platform to isolate high-risk documents automatically, routing them to the correct operational queues through exception workflows. For a platform like DocVu.AI, automated anomaly detection is not a siloed tool, but a natural extension of its core validation and exception management capabilities. By integrating these risk checks directly into the primary ingestion pipeline, the system handles document intelligence and workflow acceleration simultaneously. Lenders can pinpoint data anomalies early in an intuitive interface, accelerating overall file readiness without disrupting their core underwriting infrastructure.

AI Signals Versus Human Judgment

To maintain operational safety and regulatory alignment, mortgage lenders must maintain a clear separation between automated signals and human decisions. The following table highlights how responsibilities are distributed between AI capabilities and human risk teams: