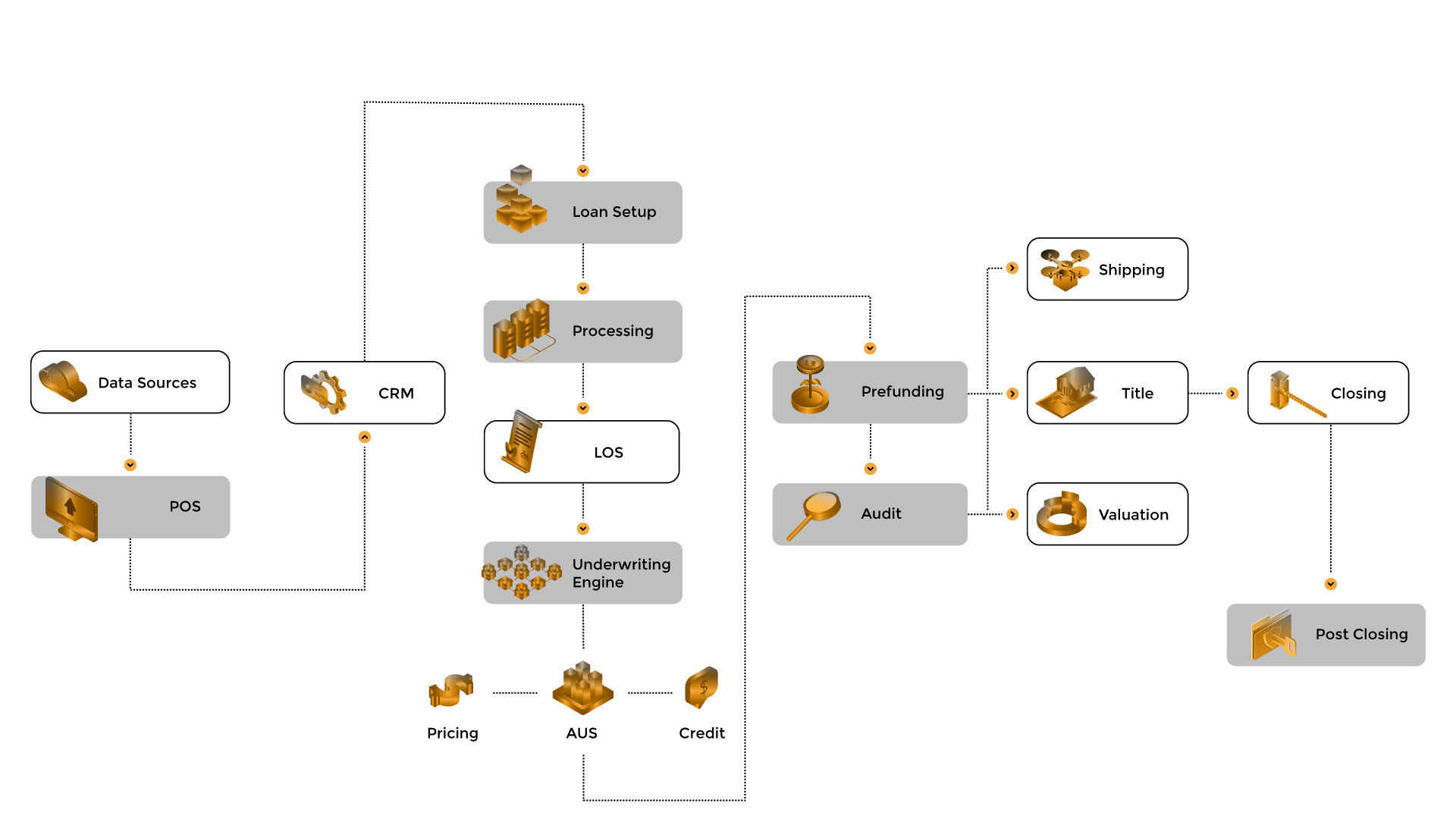

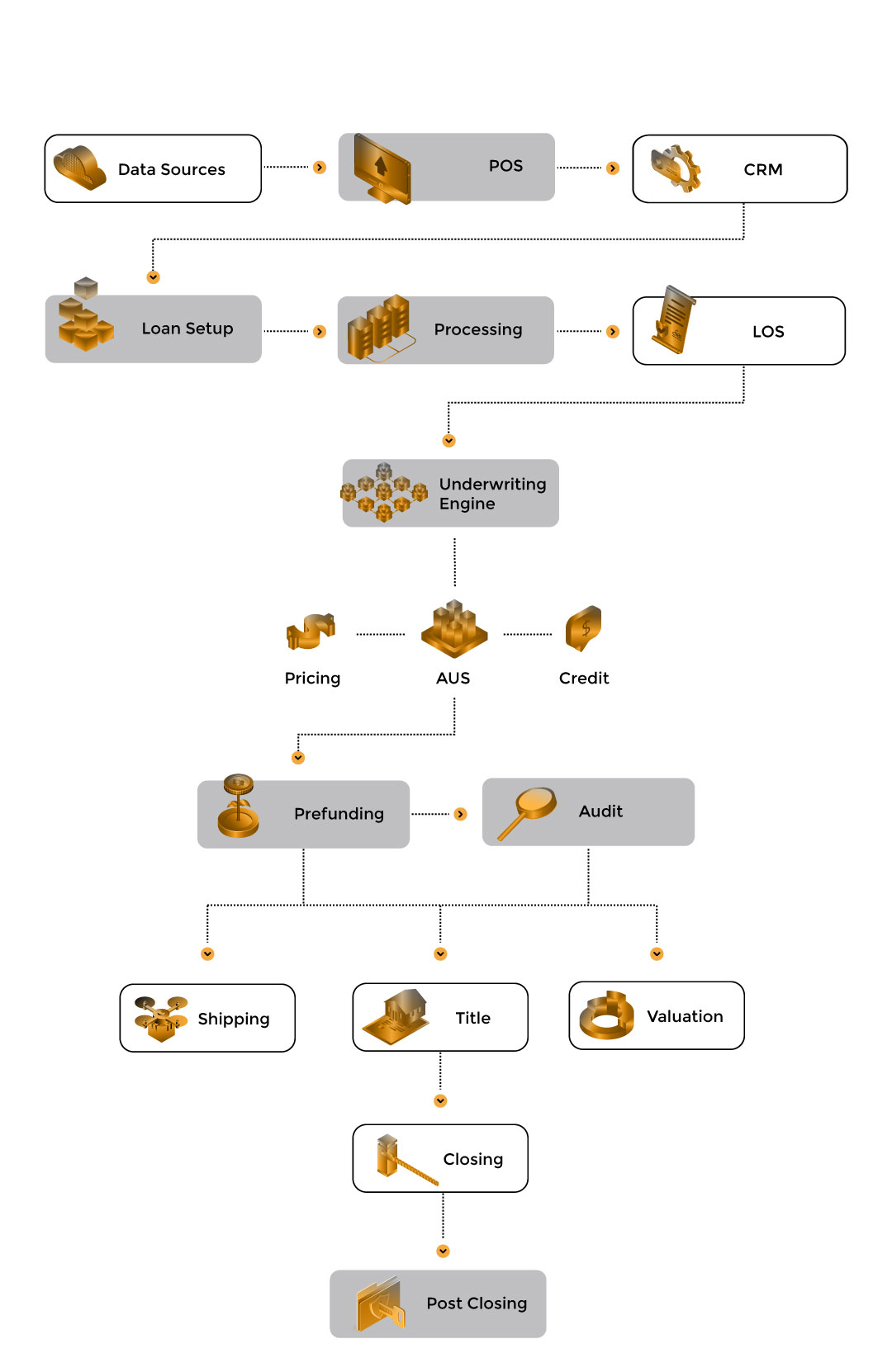

Applications based mortgage

Leverages AI-based engines to improve document processing capabilities with enhanced speed and accuracy

Mortgage underwriting

Utilizes the AI engine to simplify mortgage underwriting to provide the accurate and relevant information for the underwriters to take a faster decision and save cost.

Mortgage Appraisals and Valuation

Analyze mortgage valuations with more precision and helping faster processing of mortgage documents.

Reporting and Analysis

Reports anomalies and information gaps with increased efficiency and improve submission of compliance reports such as HMDA

Case Studies

How DocVu.AI Revolutionized ‘Order to Cash Process’ for a Leading Pharma Chain

Please submit this form to download Case Study

Case Studies

Bank in North America to Achieve Excellence in Post-Close Audit using IDP solutions

Please submit this form to download Case Study

Article

Top 7 Document Hurdles in Non-QM Lending, solved by DocVu.AI.

In today’s lending landscape, borrower profiles are no longer uniform, and neither are their documents. As Non-QM lending becomes a

Article

How Intelligent Document Processing (IDP) is Revolutionizing Enterprise Workflows

In today’s fast-paced digital world, businesses face the constant pressure to optimize efficiency, reduce costs, and stay ahead of the

Article

Top 6 Pain Points in Mortgage Document Management and How DMSVu Fixes Them

In mortgage lending, document management has become a quiet drag on performance. From intake to audit, teams deal with scattered